---

title: Wildfires, Insurer Withdrawal, and the Expansion of FAIR Plans in California

subtitle: Data Analytics Capstone Project

author:

- name: Ann Brennan

affiliation: SUNY Geneseo

date: last-modified

execute:

echo: true

eval: true

warning: false

message: false

fig-width: 10

fig-height: 6

format:

html:

code-fold: true

toc: true

toc-title: "Contents"

toc-expand: 3

number-sections: true

code-tools: true

highlight-style: atom-one

editor:

markdown:

wrap: 72

---

```{r setup}

#| include: false

library(sf)

library(ggplot2)

library(dplyr)

library(tidyr)

library(tigris)

library(viridis)

library(stargazer)

library(tidyverse)

library(fixest)

library(skimr)

library(hrbrthemes)

library(modelsummary)

theme_set(theme_ipsum()+

theme(strip.background =element_rect(fill="lightgray"),

axis.title.x =

element_text(angle = 0,

size = rel(1.33),

margin = margin(10,0,0,0)),

axis.title.y =

element_text(angle = 90,

size = rel(1.33),

margin = margin(0,10,0,0))

)

)

```

```{r visualizations}

#| include: false

df <- read.csv("C:/Users/15856/Documents/merged-dataset-clean.csv")

# 1. Wildfires, Non-Renewals, and FAIR Plan Enrollment Over Time

# aggregate by year

time_data <- df |>

group_by(year) |>

summarize(

wildfire = sum(acres_burned, na.rm = TRUE),

nonrenewal = sum(voluntary_non_renewed_insurer_initiated, na.rm = TRUE),

fair = sum(fair_policies, na.rm = TRUE)

)

# standardize variables

time_data <- time_data |>

mutate(

wildfire_scaled = scale(wildfire),

nonrenewal_scaled = scale(nonrenewal),

fair_scaled = scale(fair)

)

# reshape to long format

time_long <- time_data |>

select(year, wildfire_scaled, nonrenewal_scaled, fair_scaled) %>%

pivot_longer(

cols = -year,

names_to = "variable",

values_to = "value"

)

# rename variables

time_long$variable <- recode(time_long$variable,

wildfire_scaled = "Wildfire Activity",

nonrenewal_scaled = "Non-Renewals",

fair_scaled = "FAIR Plans"

)

# 2. Maps - Wildfires, Non-Renewals, and FAIR Plans (2021)

# load shapefile for ca counties

ca_counties <- st_read("C:/Users/15856/Downloads/ca_counties/CA_Counties.shp")

# enable cache

options(tigris_use_cache = TRUE)

# filter - only 2021 data

data_2021 <- df |>

filter(year == 2021)

# check county names before merging

unique(ca_counties$NAME)[1:10]

unique(df$county)[1:10]

# standardize county names for merging

ca_counties <- ca_counties |>

mutate(NAME = toupper(NAME))

# merge data with shapefile

map_data <- ca_counties |>

left_join(data_2021, by = c("NAME" = "county"))

# create log transformed variables and rename

map_data <- map_data |>

mutate(

wildfire = log(acres_burned_lag1 + 1),

fair = log_fair_policies,

nonrenewal = log(voluntary_non_renewed + 1)

)

# reshape data

map_long <- map_data |>

select(NAME, geometry, wildfire, fair, nonrenewal) %>%

pivot_longer(

cols = c(wildfire, fair, nonrenewal),

names_to = "variable",

values_to = "value"

)

# rename variables for visual

map_long$variable <- recode(map_long$variable,

wildfire = "Wildfire (Log Acres Burned, Lagged)",

fair = "FAIR Plan Policies (Log)",

nonrenewal = "Non-Renewals (Log)"

)

# standardize variables

map_long <- map_long |>

group_by(variable) |>

mutate(value_scaled = scale(value)) %>%

ungroup()

```

```{r models}

#| include: false

# ------- FE Panel Regression --------------

# Outcome variable: log FAIR Plans

# log transformation

df <- df |>

mutate(

log_acres_burned = log(acres_burned + 1),

log_non_renewed = log(voluntary_non_renewed_insurer_initiated + 1)

)

# run model

model <- lm(

log_fair_policies ~ log_acres_burned +

log_non_renewed +

median_income +

housing_units +

median_home_value +

factor(county) + factor(year),

data = df

)

# Outcome variable: log Non-Renewals

# log transformation

df <- df |>

mutate(

log_acres_burned = log(acres_burned + 1),

log_non_renewed = log(voluntary_non_renewed_insurer_initiated + 1)

)

# run model

model2 <- lm(

log_non_renewed ~ log_acres_burned +

median_income +

housing_units +

median_home_value +

factor(county) + factor(year),

data = df

)

# -------- Linear Regression ---------------

## Outcome variable: log FAIR Plans

# year fe model

model_year_fe <- feols(

log(fair_policies) ~ log(acres_burned_lag1) + log(voluntary_non_renewed_insurer_initiated) +

median_income + housing_units + median_home_value | year,

data = df

)

# county fe model

model_county_fe <- feols(

log(fair_policies) ~ log(acres_burned_lag1) + log(voluntary_non_renewed_insurer_initiated) +

median_income + housing_units + median_home_value | county,

data = df

)

# two-way fe model

model_both_fe <- feols(

log(fair_policies) ~ log(acres_burned_lag1) + log(voluntary_non_renewed_insurer_initiated) +

median_income + housing_units + median_home_value | year + county,

data = df

)

# set seed

set.seed(123)

# split train/test

train_data <- df[df$year < 2020, ]

test_data <- df[df$year >= 2020, ]

# train model

model_test <- feols(

log(fair_policies + 1) ~ log(acres_burned_lag1 + 1) +

log(voluntary_non_renewed_insurer_initiated + 1) +

median_income + housing_units + median_home_value | county,

data = train_data

)

# generate predictions

preds <- predict(model_test, newdata = test_data)

# actual values

actual <- log(test_data$fair_policies + 1)

```

# Introduction

In recent years, wildfires have become more frequent and severe across

the western United States, particularly in California. This has

contributed to growing economic costs for households, insurers, and

policymakers. These events have also begun to reshape the functioning of

private insurance markets in California. As wildfire risk increases,

insurers face rising claims and uncertainty, causing many to reassess

their exposure in high-risk areas. This is visible in an increase of

policy non-renewals. This means insurers choose not to continue coverage

for existing customers. This shift raises concerns about access to

insurance and the stability of housing markets in wildfire-prone areas.

Homeowners who are unable to obtain or maintain private coverage must

turn to alternative options. The most prominent alternative is

California’s FAIR (Fair Access to Insurance Requirements) Plan. The FAIR

Plan is a state-mandated insurer of last resort designed to provide

basic property insurance to high-risk properties that cannot acquire

coverage in the private market. It serves as an important safety net,

however, FAIR Plan coverage is typically more expensive and offers

limited protection compared to standard policies. As a result, increased

reliance on the FAIR Plan may signal instability in the insurance market

and create financial burdens for homeowners.

This project examines the relationship between wildfire activity,

insurer behavior, and the expansion of FAIR Plan coverage in California.

The primary research question is: **How does wildfire activity affect

insurer non-renewals, and how do non-renewals drive FAIR Plan growth?**

This question aims to help understand how climate-related risks

translate into market outcomes and policy challenges.

To answer this question, this study uses a county-year level dataset

covering all 58 counties in California from 2015 to 2021. This dataset

combines information from multiple data sources, including the

California Department of Insurance (CDI), which provides data on insurer

non-renewals and FAIR Plan policy counts. It also includes Cal Fire,

which provides measures of wildfire activity such as acres burned, and

the U.S. Census Bureau, which contributes socioeconomic controls

including housing units, median home value, and median income. The unit

of observation is county-year, allowing for analysis of changes within

counties over time while accounting for differences across regions.

The main empirical methods will be a fixed effects panel regression and

linear regression model. These models will be used to estimate

relationships between the variables of interest. County fixed effects

control for time-invariant characteristics such as geography, baseline

fire risk, and existing economic conditions. Year fixed effects control

for statewide shocks, including severe wildfire seasons or changes in

state insurance requirements. By isolating variation within counties,

this framework focuses on the effect of changing wildfire activity on

insurer non-renewals and their subsequent impact on FAIR Plan

enrollment. This analysis aims to provide more credible estimates of

these relationships by concentrating on variation within counties over

time.

The results of this analysis indicate that increased wildfire activity

may be associated with higher insurer non-renewals. This suggests that

insurers reduce their exposure in response to greater risk.

Additionally, higher non-renewal rates are associated with increased

FAIR Plan enrollment. This indicates that homeowners who lose their

private coverage turn to the FAIR Plan as an insurer of last resort.

Overall, the results suggest that climate-related risk is pushing

homeowners away from private insurance and toward FAIR Plan coverage.

However, there are significant trade-offs associated with this shift, as

FAIR Plan policies are often more expensive with less coverage.

The findings of this project have important implications for multiple

stakeholders. For the insurance industry, the results highlight the

challenges of maximizing profits and managing risk with increasingly

severe wildfire incidents. For policymakers, the expansion of FAIR Plan

enrollment suggests that the program is functioning as intended for the

short-term, however, this is not a long-term solution. The FAIR Plan

program is intended as a temporary safety net, and may not be

sustainable if homeowners continue to increase reliance on it. For

housing markets, rising non-renewals and higher insurance costs may

reduce property values, limit mortgage availability, and reduce housing

availability in high-risk areas. Overall, this project contributes to

the understanding of how environmental risk is associated with and

translates to market changes and policy responses. It also provides

evidence that can inform future decisions about insurance regulation,

climate risk management, and housing policy in wildfire-prone regions.

# Background and Related Literature

Wildfire risk has become an increasingly important issue for insurance

markets in California. As wildfires have become more frequent and severe

over time, the cost of insuring high-risk properties has increased. This

impacts and creates challenges for insurers, policymakers, and

homeowners. In response to increased wildfire risk, insurers may

increase premiums or completely withdraw from high-risk areas. When

homeowners lose or cannot obtain private insurance, they often rely on

“insurers of last resort”, such as California’s FAIR Plan. This state

mandated program provides basic coverage to high-risk properties to

ensure homeowners can still meet mortgage and legal requirements.

Prior research shows that wildfire risk generates significant economic

costs with implications for housing, land use, and risk management.

Literature by Bayham et al. (2022) provides a comprehensive review of

the economics of wildfires in the United States, documenting the scale

of damage and incentive challenges in high-risk areas. At the same time,

work by Boomhower, Fowlie, and Plantinga (2023), shows that insurance

markets also shape risk mitigation behavior. A key finding is that

insurer discounts for risk mitigation can help households learn about

ways to reduce their own losses. This suggests that insurance influences

how people respond to risk.

More recent work focuses on how climate risk is reshaping housing

insurance markets. Keys and Mulder (2025) show that increased climate

disaster risk is reflected in insurance and mortgage data, with insurers

adjusting coverage and pricing in response to perceived risk and

exposure in the long run. Similarly, Fowlie et al. (2025) highlight that

climate change is affecting home insurance markets through rising

premiums, coverage restrictions, and insurer withdrawal in high-risk

areas. These findings support the idea that insurance markets may become

less stable as climate risk increases.

California’s FAIR Plan is generally viewed as an important safety net,

but also interpreted as a signal of instability in the private insurance

market. Auer (2024) emphasizes that as wildfire risk increases, insurers

have started to restrict coverage or exit high-risk areas, which has

important implications for both policymakers and homeowners. Overall,

this literature suggests that insurer behavior plays a key role in how

wildfire risk translates to insurance access.

Important gaps still remain in the existing research. Most of the

existing literature focuses on either insurance pricing or broad market

outcomes, with less emphasis on specifically how non-renewals connect

wildfire exposure to the expansion of insurers of last resort.

Additionally, there is limited county-level evidence linking wildfire

activity, insurer withdrawal, and FAIR Plan enrollment over time. This

project contributes to existing literature by using a county-year panel

dataset to examine the relationship between wildfire activity, insurer

non-renewals, and FAIR Plan growth in California. This provides more

evidence on the role of insurer behavior as a connection between climate

risk and insurance market outcomes.

# Data

## Data Sources

This analysis combines data from three primary sources to create a

county-level panel dataset with wildfire activity, insurance policy

outcomes, and socioeconomic features in California. First, the data on

insurer non-renewals and FAIR policy counts are obtained from the

California Department of Insurance (CDI). The CDI collects this

information to monitor insurer behavior. Their goal is to protect

consumers and keep the insurance market stable. This data provides

annual counts of non-renewed policies, as well as new and renewed FAIR

Plan policies at the county level.

Second, wildfire activity data is collected from the California

Department of Forestry and Fire Protection (Cal Fire). This dataset

includes measures of wildfire severity in California, such as total

acres burned per county and year. Cal Fire collects this data for fire

management, risk assessment, and public reporting purposes. It is a

widely used source for analysis on wildfires.

Third, socioeconomic characteristics are obtained from the U.S. Census

Bureau, specifically the American Community Survey (ACS). The ACS

provides annual estimates on features such as median household income,

median home value, and total housing units. These variables are included

to control for differences in economic conditions and housing markets

across counties in California.

All three datasets were accessed online in March of 2026 and merged by

county and year. The new dataset allows for a comprehensive analysis of

how the relationships between wildfire risk, insurer behavior, and

socioeconomic characteristics change over time.

## Unit of Observation

The unit of observation in this project is the **county-year**. Each row

in the dataset represents one California county observed in a given

year. The dataset includes 58 counties observed over the period from

2015 through 2021. The final panel contains 438 observations.

## Sample and Scope

The sample includes all 58 counties in California over the period from

2015 through 2021. This time frame captures multiple major wildfire

seasons in order to analyze the relationship between wildfire risk and

insurance market outcomes. The dataset includes three different variable

categories: insurance market outcomes (non-renewals and FAIR Plan

policies), wildfire activity (acres burned), and socioeconomic controls

(income, home value, and housing units). The final dataset is structured

as a county-year panel, where each observation corresponds to a specific

county in a given year.

## Data Cleaning

In order to construct the final dataset, it is necessary to clean and

filter the data. First, wildfire data is spatially joined with

California county boundaries using geographic information system (GIS)

methods. Each wildfire perimeter is assigned to the counties it

intersects in order to link fires with specific geographic areas. The

fire-level data is then aggregated to the county-year level by summing

the total acres burned and summing the number of fires.

Second, the wildfire dataset is filtered to include only the years 2014

through 2021. The year 2014 is included to construct a one year lag of

wildfire activity, specifically acres burned lagged by one year. This

approach links each year’s wildfire exposure to insurer behavior in the

following year. The lag structure reflects the fact that insurers do not

respond immediately. Instead, they typically adjust their policies in

the subsequent plan year after observing wildfire losses from the prior

year.

Third, missing values for acres burned and number of fires are replaced

with zeros. Counties with zero wildfire activity are still included in

the dataset, serving as a baseline group for the analysis.

Next, insurance data from the California Department of Insurance is

cleaned and transformed. County identifiers are standardized, and

character variables are converted to numeric format where necessary.

FAIR Plan coverage is constructed by combining the number of new and

renewed FAIR Plan policies into a single measure of total FAIR Plan

policies. It is important to note that the number of non-renewals are

insurer initiated, and exclude those initiated by consumers to

exclusively reflect insurer behavior.

Additionally, socioeconomic control variables are obtained from the

American Community Survey and reshaped into the county-year panel

format. The control variables are merged with the insurance and wildfire

datasets using consistent county-year identifiers.

Finally, a few key variables are transformed for analysis. Log

transformations are applied to skewed variables including FAIR Plan

policies, lagged acres burned, and non-renewals.

## Key Variables

The primary outcome variables in this analysis aim to capture both

insurer behavior and reliance on an insurer of last resort. The first

outcome, insurer non-renewals, is measured as the number of policies not

renewed by insurers in a given county-year. The second outcome, FAIR

Plan policies, is the sum of new and renewed FAIR Plan policies. This

represents a total count of participation in the FAIR Plan. The main

explanatory variable is wildfire activity, which is measured as total

acres burned in a county-year. A lagged version of this variable is used

to reflect the timing of insurer responses. Insurer non-renewals are

also included as an explanatory variable when the outcome is FAIR Plan

policies. Control variables include median household income, median home

value, and total housing units. These variables account for differences

in economic conditions and housing markets across different counties.

## Data Quality and Limitations

Although this dataset is constructed from credible administrative

sources, it is important to note its limitations. First, the measure of

wildfire activity is solely based on total acres burned, which may not

fully represent perceived wildfire risk or expected future losses. For

example, insurers may respond to other variables such as proximity to

fires or anticipated risk rather than just realized damage.

Additionally, spatially assigning fires to counties based on geographic

overlap may cause measurement error, particularly for fires that spread

to multiple counties. Second, the insurance data does not include

information on premiums, underwriting criteria, or specific policy

characteristics. Because of this, the analysis does not reflect pricing

adjustments or changes in policy terms, which are notable insurer

behaviors. Third, the sample size is limited to 58 counties over seven

years, which is a relatively small panel dataset. The limited time span

may reduce the statistical power and precision of estimates. Finally,

although this analysis controls for year and county fixed effects, the

results should be interpreted as identifying strong associations rather

than definitive causal effects. Additional factors, such as policy

changes or unobserved insurer strategies, may influence the

relationships between variables.

## Data Dictionary

**fair_policies**

Number of policies enrolled in the California FAIR Plan (county-year

level).

**acres_burned_lag1**

Total acres burned by wildfires in the previous year (one-year lag).

**voluntary_non_renewed_insurer_initiated**

Number of insurance policies not renewed by insurers (excluding

consumer-initiated cancellations).

**median_income**

Median household income in the county (in dollars). Controls for local

economic conditions.

**housing_units**

Total number of housing units in the county. Controls for county size

and amount of housing.

**median_home_value**

Median value of owner-occupied housing units (in dollars). Controls for

housing market conditions.

**log_fair_policies**

Natural log of FAIR Plan policies. Used to reduce skewness.

**log_acres_burned**

Natural log of wildfire acres burned. Used to reduce skewness.

**log_non_renewed**

Natural log of insurer-initiated non-renewals. Used to reduce skewness.

## Summary Statistics

```{r summary-statistics}

df |>

select(

fair_policies,

acres_burned_lag1,

voluntary_non_renewed_insurer_initiated,

median_income,

housing_units,

median_home_value

) |>

skim()

```

# Empirical Strategy / Methods

## Empirical Approach

This analysis uses a combination of fixed effects panel regression and

linear regression models to examine the relationship between wildfire

activity, insurer non-renewals, and FAIR Plan enrollment. The primary

goal is to estimate how changes in wildfire exposure influence insurer

behavior, and in turn, how insurer withdrawal affects the reliance on

California’s FAIR Plan. A fixed effects structure is suitable for this

analysis because the dataset consists of observations from the same

counties over time. Counties differ in many ways, such as geography,

baseline wildfire risk, and housing market structure. These differences

may influence wildfire exposure and insurance outcomes. The model’s

county fixed effects control for these time invariant differences across

counties. Year fixed effects are included to control for statewide

shocks that would impact all counties in a given year, such as

particularly severe wildfire seasons or changes in state insurance

regulations. Additionally, a predictive modeling component is

implemented using a train-test split to evaluate out of sample

performance. This assesses how well the model can predict FAIR Plan

enrollment and insurer non-renewals based on observed variables.

## Model Specification

The primary empirical model estimates the relationship between wildfire

activity, insurer non-renewals, and FAIR Plan enrollment using a two-way

fixed effects panel regression. The outcome variable is the logarithm of

FAIR Plan policies at the county-year level. The use of a logarithm

reduces skewness while still capturing proportional changes in

relationships in FAIR Plan enrollment.

$\log({FAIR\_policies}_{it})$ $=$

$\beta_0$ $+$ $\beta_1 \log({acres\_burned}_{i,t-1})$ $+$

$\beta_2 \log({non\_renewals}_{it})$ $+$

$\beta_3 X_{it}$ $+$ $\alpha_i$ $+$ $\gamma_t$ $+$ $\varepsilon_{it}$

In this model specification, $i$ indexes counties and $t$ indexes years.

The outcome variable is the log of FAIR Plan policies in county $i$ at

time $t$. The main explanatory variables are the log of acres burned in

the previous year and the log of insurer initiated non-renewed policies.

The vector $X_{it}$ includes three control variables: median household

income, housing units, and median home value. County fixed effects

($\alpha_i$) control for time invariant county characteristics. Year

fixed effects ($\gamma_t$) control for statewide shocks impacting all

counties in a given year. The error term is denoted by

$\varepsilon_{it}$.

Additionally, alternative specifications are estimated using different

combinations of fixed effects, including models with only year fixed

effects, only county fixed effects, and both. This helps evaluate how

sensitive the results are to different sources of variation.

## Additional Outcome: Insurer Non-Renewals

This analysis also examines insurer behavior directly by estimating

models with insurer non-renewals as the outcome variable. In these

specifications, lagged wildfire activity is the primary explanatory

variable. This helps evaluate whether wildfire risk leads insurers to

withdraw from high-risk markets. This two step approach first links

wildfire activity to non-renewals and then links non-renewals to FAIR

Plan growth, which provides a more complete picture of how environmental

risk affects insurance market outcomes.

## Prediction and Model Evaluation

In addition to the panel regression analysis, a predictive modeling

technique is conducted using a train-test split. The dataset is divided

into a training sample (2015-2019) and a testing sample (2020-2021). The

linear regression model is estimated on the training data and then used

to generate predictions for FAIR Plan enrollment in the testing time

period. Model performance is evaluated using the root mean squared error

(RMSE). RMSE measures the average magnitude of errors in the prediction.

Lower RMSE values indicate better accuracy in the model’s predictions.

This approach helps show how well the model performs on new data and

whether the relationships found in the regression are useful for

prediction.

## Interpretation and Identification

The coefficients in the regression models are interpreted as

correlations between variables rather than causal effects. For example,

the coefficient for lagged acres burned represents the relationship

between changes in wildfire activity and changes in FAIR Plan enrollment

within a county, holding other factors constant. Including county and

year fixed effects strengthens the analysis by controlling for

unobserved differences across counties and state-wide trends over time.

However, this analysis does not use an empirical model that supports

causal claims. The results should be interpreted as showing

correlational relationships, not causal effects.

# Results

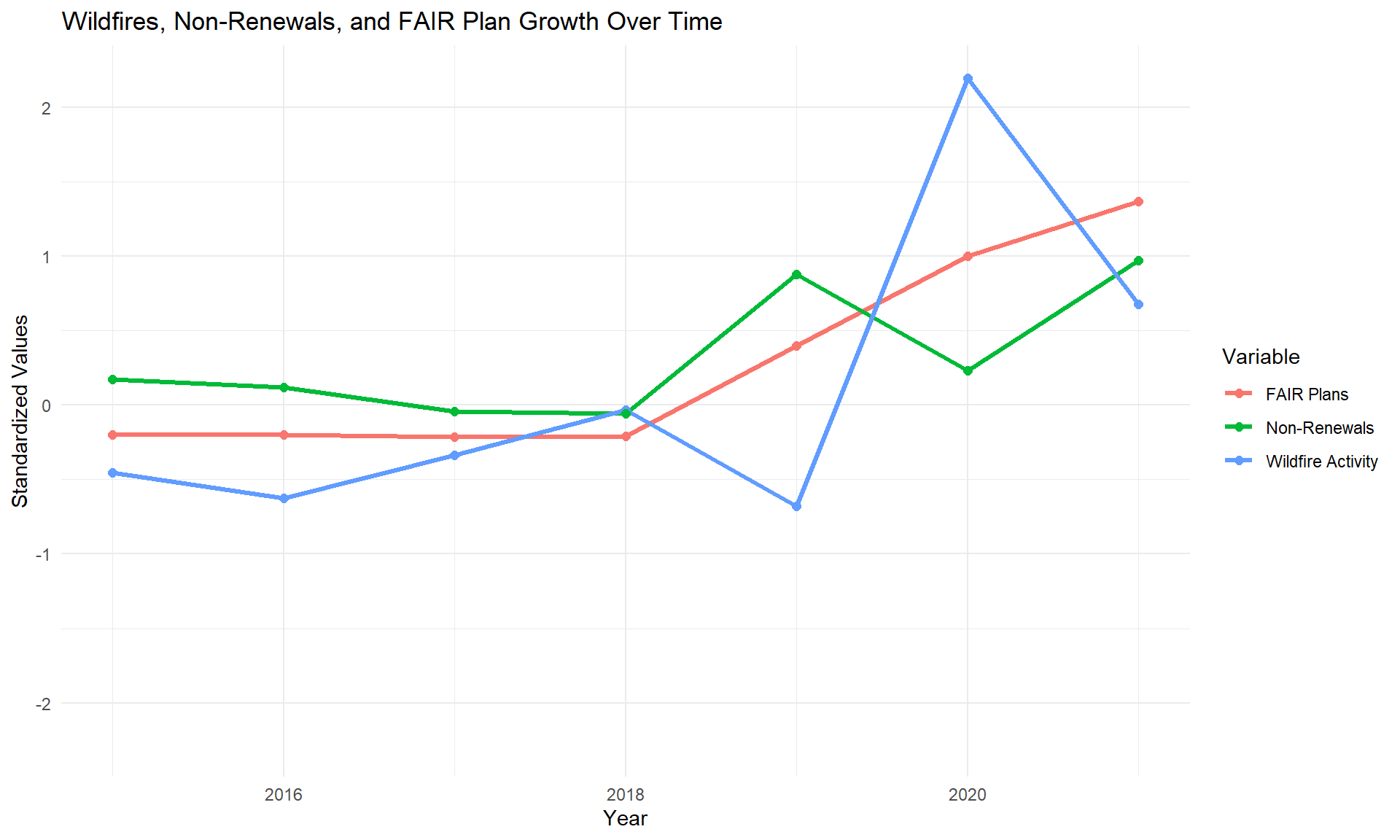

## Figure 1: Wildfire Activity, Insurer Non-Renewals, and FAIR Plan Enrollment Over Time

```{r results-figure-1}

ggplot(time_long, aes(x = year, y = value, color = variable)) +

geom_line(size = 1.2) +

geom_point(size = 2) +

labs(

title = "Wildfires, Non-Renewals, and FAIR Plan Growth Over Time",

x = "Year",

y = "Standardized Values",

color = "Variable"

) +

theme_minimal()

```

Figure 1 shows a clear pattern over time linking wildfire severity to

insurance market responses. Wildfire activity shows variation over time,

with a large spike in 2020. This reflects one of the most severe

wildfire seasons for California in recent history. This spike is

followed by noticeable increases in both insurer non-renewals and FAIR

Plan enrollment during the following year.

A key pattern in this graph is the lag between wildfire exposure and

insurer behavior. Wildfire activity peaks in 2020, but increases in

non-renewals do not occur until the following year. This is consistent

with the idea that insurers make decisions after observing losses.

Through this lag structure, policy decisions are typically made

annually.

At the same time, FAIR Plan enrollment shows a steady upward trend

throughout the period from 2015 through 2021. This suggests that as

private insurers reduce the number of policies in high-risk areas,

homeowners increasingly rely on FAIR Plan policies as an alternative

form of coverage. These patterns provide initial visual evidence of

interconnected relationships between the key variables: as wildfire risk

increases, insurers withdraw from the market, and FAIR Plan coverage

increases.

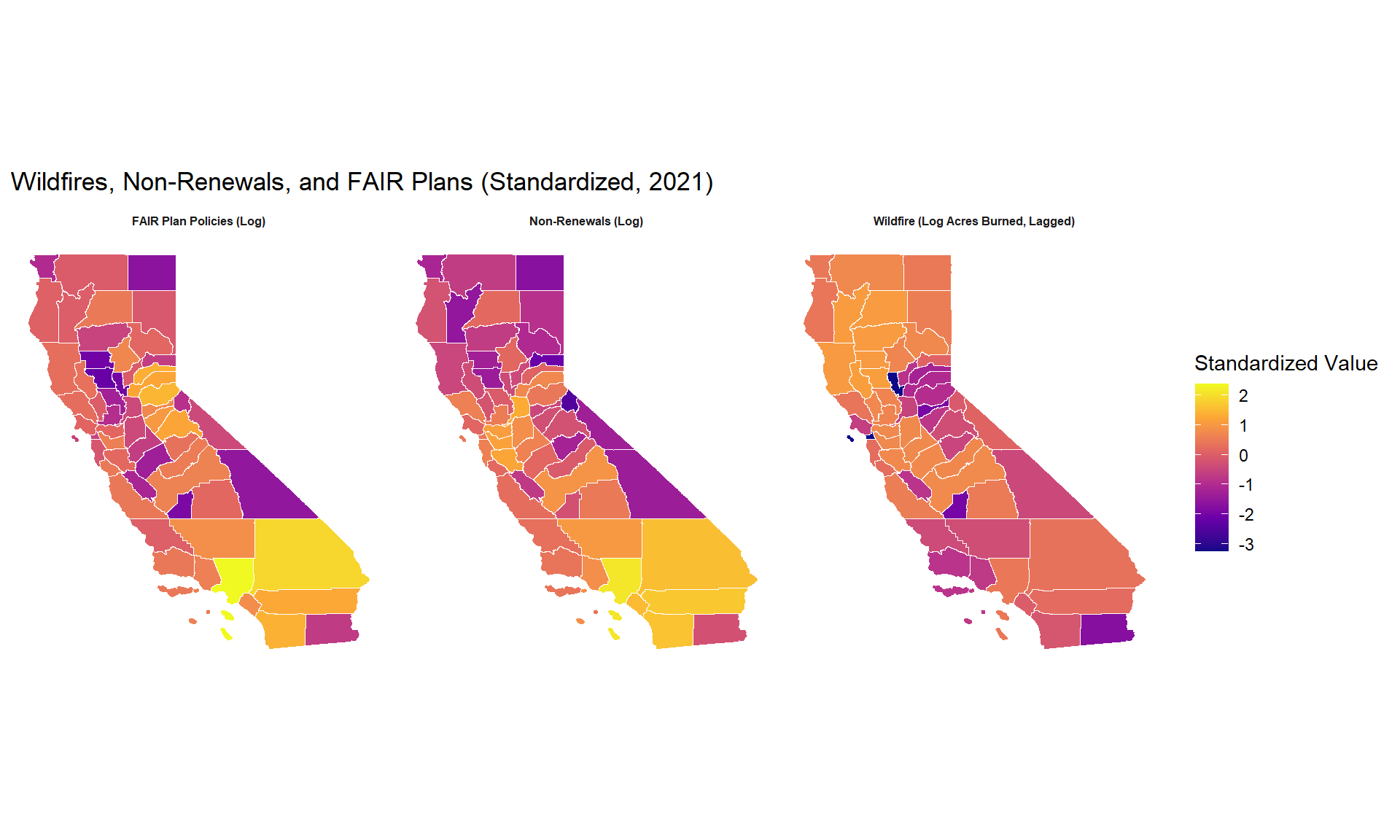

## Figure 2: Geographic Distribution of Wildfire Activity, Insurer Non-Renewals, and FAIR Plan Enrollment in California (2021)

```{r results-figure-2}

ggplot(map_long) +

geom_sf(aes(fill = value_scaled), color = "white", size = 0.2) +

scale_fill_viridis_c(option = "plasma", na.value = "gray90") +

facet_wrap(~variable) +

labs(

title = "Wildfires, Non-Renewals, and FAIR Plans (Standardized, 2021)",

fill = "Standardized Value"

) +

theme_minimal() +

theme(

panel.grid = element_blank(),

axis.text = element_blank(),

axis.ticks = element_blank(),

strip.text = element_text(size = 6, face = "bold")

)

```

Figure 2 shows the geographic distribution of wildfire activity, insurer

non-renewals, and FAIR Plan enrollment across California counties in

2021. The maps use a color gradient, with darker colors (purple and dark

orange) indicating higher values and lighter colors (yellow and light

orange) indicating lower values.

Overall, the maps show a clear spatial pattern, where counties with

higher wildfire activity also tend to have higher non-renewals and

greater FAIR Plan enrollment. These patterns are concentrated in

high-risk areas instead of being evenly distributed across the state.

This alignment suggests that insurer withdrawal is concentrated in areas

with greater wildfire exposure. FAIR Plan enrollment is also highest in

the same counties, indicating that the FAIR Plan is being used where

private coverage is reduced.

## Primary Fixed Effects Regression Results

```{r results-table-1}

stargazer(model,

type = "text",

title = "Fixed Effects Regression Results",

dep.var.labels = "Log(FAIR Policies)",

covariate.labels = c("Log(Acres Burned, Lagged)",

"Log(Non-Renewals)",

"Median Income",

"Housing Units",

"Median Home Value"),

omit = c("factor"),

digits = 3)

```

The primary fixed effects panel regression examines how wildfire

activity and insurer non-renewals affect FAIR Plan enrollment at the

county-year level. It controls for county and year fixed effects as well

as socioeconomic variables.

The key result is a strong and statistically significant relationship

between insurer non-renewals and FAIR Plan enrollment. A 1% increase in

non-renewals is associated with approximately a 1.26% increase in FAIR

Plan policies, holding all other factors constant. This suggests a

strong substitution effect between private insurance and the FAIR Plan.

On the other hand, wildfire activity (lagged acres burned) is not

statistically significant once insurer behavior and the fixed effects

are included. This suggests that wildfire exposure does not directly

translate into FAIR Plan growth, but may affect it indirectly through

insurer decisions.

## Alternative Specification: Insurer Non-Renewals as Outcome Variable

```{r results-table-2}

stargazer(model2,

type = "text",

title = "Fixed Effects Regression Results",

dep.var.labels = "Log(Non-Renewals)",

covariate.labels = c("Log(Acres Burned, Lagged)",

"Log(FAIR Policies)",

"Median Income",

"Housing Units",

"Median Home Value"),

omit = c("factor"),

digits = 3)

```

Additionally, insurer non-renewals are used as the outcome variable to

examine whether wildfire activity is directly associated with insurer

withdrawal behavior. FAIR Plan enrollment is not included in this model.

In this model, lagged wildfire activity is statistically significant, but the effect is very small. The coefficient of -0.009 suggests that a 1% increase in lagged acres burned is associated with a 0.009% decrease in insurer non-renewals, holding other factors constant. Although statistically significant, the magnitude of this effect is quite small. When combined with earlier results showing weak and insignificant effects of wildfire activity, this suggests that wildfire exposure does not have a strong direct relationship with insurance outcomes. Overall, this shows that wildfires mainly affect the insurance market through how insurers respond, rather than a direct impact on insurance outcomes.

## Predictive Model Results - Linear Regression

```{r results-table-3}

etable(model_year_fe, model_county_fe, model_both_fe)

```

```{r}

rmse <- sqrt(mean((actual - preds)^2, na.rm = TRUE))

rmse

```

A linear regression model is also used to assess how well the variables

explain FAIR Plan enrollment. Three baseline models are estimated using

only year fixed effects, only county fixed effects, and both fixed

effects. Insurer non-renewals are consistently the strongest predictor

of FAIR Plan enrollment across all three models.

Wildfire activity is not statistically significant in any of the models. This reinforces the earlier results showing a weak direct relationship between wildfire exposure and FAIR Plan enrollment once fixed effects are included. The model fit improves when county fixed effects are added, indicating that differences across counties are important in explaining the model results.

The model is then evaluated using a train-test split (2015-2019 for training and 2020-2021 for testing). The resulting root mean squared error (RMSE) is 1.003. This indicates moderate predictive accuracy. Overall, the predictive model results reinforce the main findings from the fixed effects regression. Non-renewals are directly correlated with FAIR Plan enrollment, while wildfire activity shows a much weaker direct relationship.

# Discussion and Implications

The results suggest that insurer non-renewals are the primary driver of

FAIR Plan enrollment. Wildfire risk may be an underlying factor,

however, its direct effect is weak or inconsistent once county and year

fixed effects are included. The strongest and most consistent

relationship is between non-renewals and FAIR Plan growth. This suggests

that the impacts of wildfires are translated indirectly through insurer

behavior. Instead of responding immediately to wildfire activity,

insurers may adjust their coverage based on broader risk factors, which

leads to increased non-renewals. Households that lose private coverage

then turn to the FAIR Plan. The predictive results also support this

interpretation, as non-renewals are the strongest predictor across all

models.

These findings have important implications for insurance markets and policymakers. They suggest that changes in insurance availability are driven more by insurer responses than by wildfire activity alone. Because of this, policies focused only on reducing wildfire risk may not be sufficient to stabilize the insurance market. The results also emphasize the FAIR Plan’s growth as an insurer of last resort. As non-renewals increase, more households rely on the FAIR Plan, which is typically more expensive with limited coverage. This raises concerns about long term sustainability and access to affordable insurance, especially in high-risk areas. Overall, these findings suggest that insurer withdrawal may reflect future instability in the insurance market, not just current wildfire exposure. This emphasizes the need for policies that consider both risk levels and the factors influencing insurer decisions.

A key recommendation is that policy efforts should focus on reducing insurer non-renewals and stabilizing the private insurance market. One approach is for state regulations to require insurers to maintain coverage in high-risk areas. These regulations could help prevent sharp increases in non-renewals and reduce the number of households forced to enroll in the FAIR Plan. However, this policy change comes with significant tradeoffs. Requiring insurers to remain in high-risk areas may increase their losses, which could lead to increased premiums and reduced profitability. This approach should be used in addition to other measures, such as risk-based pricing and risk mitigation incentives, in order to stabilize the insurance market in the long run. At the same time, policymakers should prepare for continued FAIR Plan growth by potentially expanding coverage to meet demand. However, reliance on the FAIR Plan should still be limited, as it is not a substitute for a stable private insurance market.

# Conclusion

This project examines how wildfire activity affects insurer non-renewals

and how non-renewals, in turn, drive FAIR Plan growth in California. The

main research question is: **How does wildfire activity affect insurer

non-renewals, and how do non-renewals drive FAIR Plan growth?** This

question is important because increasing wildfire risk has raised

concerns about the stability of private insurance markets and the

reliance on the FAIR Plan as an insurer of last resort for homeowners in

high-risk areas. To answer this, the analysis uses a county-year panel

dataset covering all 58 counties in California from 2015 to 2021. The

dataset combines wildfire data from Cal Fire, insurance data from the

California Department of Insurance, and socioeconomic controls from the

U.S. Census Bureau. The empirical approach uses fixed effects panel

regressions with county and year fixed effects, as well as linear

regression with a train-test split to evaluate predictive performance.

The main result is that insurer non-renewals are the strongest and most

consistent predictor of FAIR Plan enrollment, while wildfire activity

has weak or statistically insignificant direct effects once fixed

effects are taken into account. These findings suggest that wildfire

risk affects insurance markets primarily through insurer behavior rather

than directly translating to insurance outcomes. Insurer withdrawal is

the main link between wildfire risk and increased reliance on the FAIR

Plan.

Overall, these results suggest that changes in insurance availability are driven by insurer responses rather than wildfire activity alone. This emphasizes the importance of policies that address insurance market participation, not just environmental risk. State efforts that reduce non-renewals or support insurer participation in high-risk areas may be effective in stabilizing the insurance market in addition to mitigating wildfire exposure. Future research could improve on this analysis by incorporating more specific data, such as zip-code or property level insurance outcomes. It could also use causal identification strategies to more clearly estimate the effect of wildfire exposure. In addition, future research could examine the role of pricing changes and regulatory policy on insurer behavior, as these factors were not directly observed in this dataset.

# References

Auer, M. R. (2024). Wildfire risk and insurance: Research directions for policy scientists. *Policy Sciences, 57*(2), 459–484.

Bayham, J., et al. (2022). The economics of wildfire in the United States. *Annual Review of Resource Economics, 14*, 379–401.

Bergé, L. (2023). *fixest: Fast fixed-effects estimations* (R package).

Boomhower, J., Fowlie, M., & Plantinga, A. J. (2023). Wildfire insurance, information, and self-protection. *AEA Papers and Proceedings, 113*, 310–315.

California Department of Forestry and Fire Protection (CAL FIRE). (n.d.). *Fire hazard severity zones*. Retrieved March 2026, from https://www.fire.ca.gov/

California Department of Insurance. (n.d.). *Data and analysis on wildfires and insurance*. Retrieved March 2026, from https://www.insurance.ca.gov/

California FAIR Plan Association. (n.d.). *Key statistics & data*. Retrieved March 2026, from https://www.cfpnet.com/

Fowlie, M., et al. (2025). *How is climate change impacting home insurance markets?* Brookings Institution.

Garnier, S. (2023). *viridis: Default color maps from 'matplotlib'* (R package).

Hlavac, M. (2022). *stargazer: Well-formatted regression and summary statistics tables* (R package).

Keys, B. (2025). *Housing, climate risk, and insurance*. NBER Working Paper.

Keys, B., & Mulder, P. (2025). *Property insurance and disaster risk: New evidence from mortgage escrow data*. NBER Working Paper.

OpenAI. (2026). *ChatGPT (GPT-5.5) [Large language model]*. Retrieved May 13, 2026, from https://chat.openai.com/

Pebesma, E. (2018). *Simple features for R: Standardized support for spatial vector data*. *The R Journal, 10*(1), 439–446.

Rudis, B. (2020). *hrbrthemes: Additional themes, theme components, and utilities for 'ggplot2'* (R package).

State of California. (n.d.). *CA geographic boundaries*.

U.S. Census Bureau. (n.d.). *American Community Survey*. Retrieved March 2026, from https://www.census.gov/

Vincent Arel-Bundock. (2023). *modelsummary: Data and model summaries in R* (R package).

Walker, K. (2023). *tigris: Load census TIGER/Line shapefiles* (R package).

Waring, E., Quinn, M., McNamara, A., Arino de la Rubia, E., Zhu, H., & Ellis, S. (2023). *skimr: Compact and flexible summaries of data* (R package).

Wickham, H. (2016). *ggplot2: Elegant graphics for data analysis*. Springer-Verlag New York.

Wickham, H. (2023). *tidyr: Tidy messy data* (R package).

Wickham, H., et al. (2019). *Welcome to the tidyverse*. *Journal of Open Source Software, 4*(43), 1686.

Wickham, H., François, R., Henry, L., & Müller, K. (2023). *dplyr: A grammar of data manipulation* (R package).